House prices are down and supply is starting to surge across much of the country.

If you’re looking to get into a property or to upsize, now could be a great time to do so. But, it would be wise to first ensure you are mortgage-savvy.

We’ve enlisted the help of mortgage expert Murray Joiner, from mortgages.co.nz, to share his wisdom.

What are some common mortgage acronyms?

If it’s your first time buying a home, it’s likely you’ll come across a host of new terms and acronyms.

Here’s a quick rundown:

What is LVR?

A loan-to-value ratio (LVR) describes the size of a mortgage compared to the total value of the property. It’s written as a percentage. Most standard mortgages need to be no more than 80% of the property’s value. That means having a deposit that’s at least 20%.

What is DTI?

The debt-to-income (DTI) ratio compares a borrower’s total debt with how much they earn. The DTI ratio is used to measure a borrower’s ability to keep up with their regular repayments.

The Reserve Bank collects this information from New Zealand’s banks and uses it to help monitor things like risk in the banking system, housing affordability, and how much general consumer spending might reduce in challenging economic times.

What is UMI?

Uncommitted monthly income (UMI) is a term used by mortgage lenders to describe how much income you have left over each month after paying for your living expenses and ‘fixed payments. Fixed payments usually include the regular repayments you make for mortgages and other debts.

What is AML?

Anti-money laundering (AML) requirements were introduced to help detect and discourage money laundering and terrorism financing. Money laundering is when money earned from illegal activity is made to look as though it came from legal sources, to help criminals cover their tracks.

If you want to know more about why these are important or how they’re calculated, Murray has written a deep dive into mortgage acronyms and terminology.

Maximise your mortgage deposits

If you’re applying for a mortgage you’ve probably been setting money aside for some time or received a significant lump sum from something like an inheritance. The more you can save for a deposit, the less risk you will be to the lender. In most cases you’ll need at least 20% of the property’s value, but there are low deposit options for first-home buyers.

Tip: Work out the difference between your current rent and the mortgage payments, council rates and house insurance premiums you expect to be paying; then pay it into your deposit savings account. This not only grows your deposit, it also helps to show a lender you can afford the expected mortgage repayments and extra costs of home ownership.

Understanding your mortgage options; Fix, float or split

Whether you’re applying for your first mortgage, restructuring an existing loan or refinancing to a new lender, it helps to understand your different mortgage options.

Spend time learning about different fix-float strategies, have a grasp of the pros and cons of each option, and how different scenarios could play out.

Fixed mortgage: A fixed interest rate doesn’t change for an agreed term.

Floating mortgage: A floating interest rate can increase or decrease at any time.

Paying off the mortgage

Committing to 20 or 30 years of debt sounds scary – don’t be deterred. Making lump sum payments can help reduce this term, and the amount that you pay.

Now that you’re in the swing of saving, keep it that way. Make a goal of paying off lump sums each year. This can accelerate the time it takes you to repay, and in turn, dramatically reduce the amount of interest you pay.

Mortgages.co.nz has a comprehensive calculator that helps you determine the impact of your lump sum payments.

Monthly Property Update

October 2022

The homes.co.nz Monthly Property Update is generated using homes.co.nz’s October 2022 HomesEstimates, providing an up-to-date perspective on house values around New Zealand.

Trends in our Main Cities

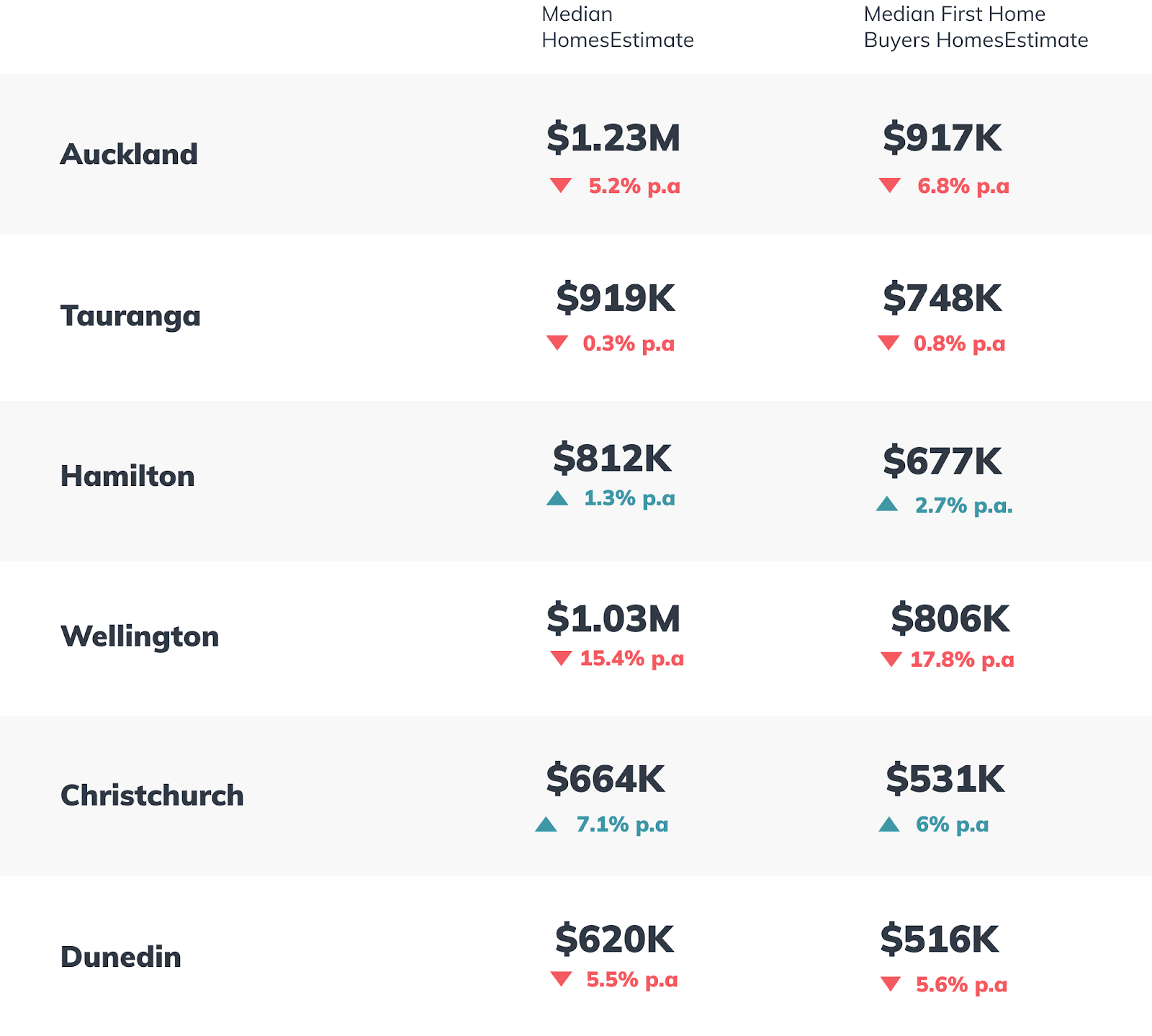

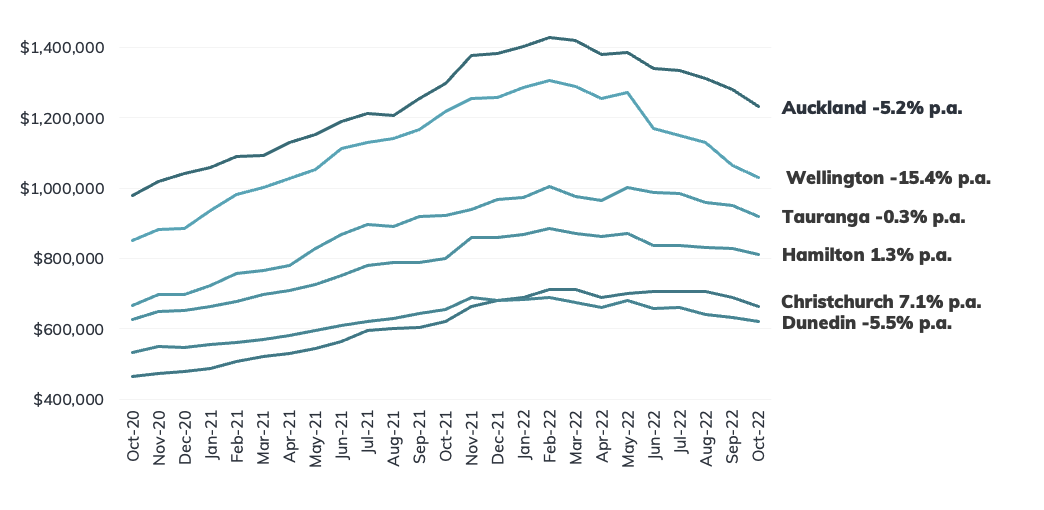

The downturn may be slowing, but there are no clear signs of it letting up, with another month-on-month decrease across the country. Christchurch and Hamilton are the only regions keeping their head above water, seeing a year-on-year increase to their median HomesEstimate.

How do we calculate these figures?

The homes.co.nz Monthly Property Update is generated using homes.co.nz’s monthly HomesEstimates and provides an up-to-date perspective on house values around New Zealand. By valuing the entire housing stock, the homes.co.nz Monthly Property Update can compare median values from month to month in a consistent and reliable way. Our HomesEstimates are calculated for almost every home in New Zealand by an algorithm that identifies the relationships between sales prices and the features of a property.

Established in 2013, homes.co.nz is NZ’s first free property information portal eager to share free property information to New Zealanders.

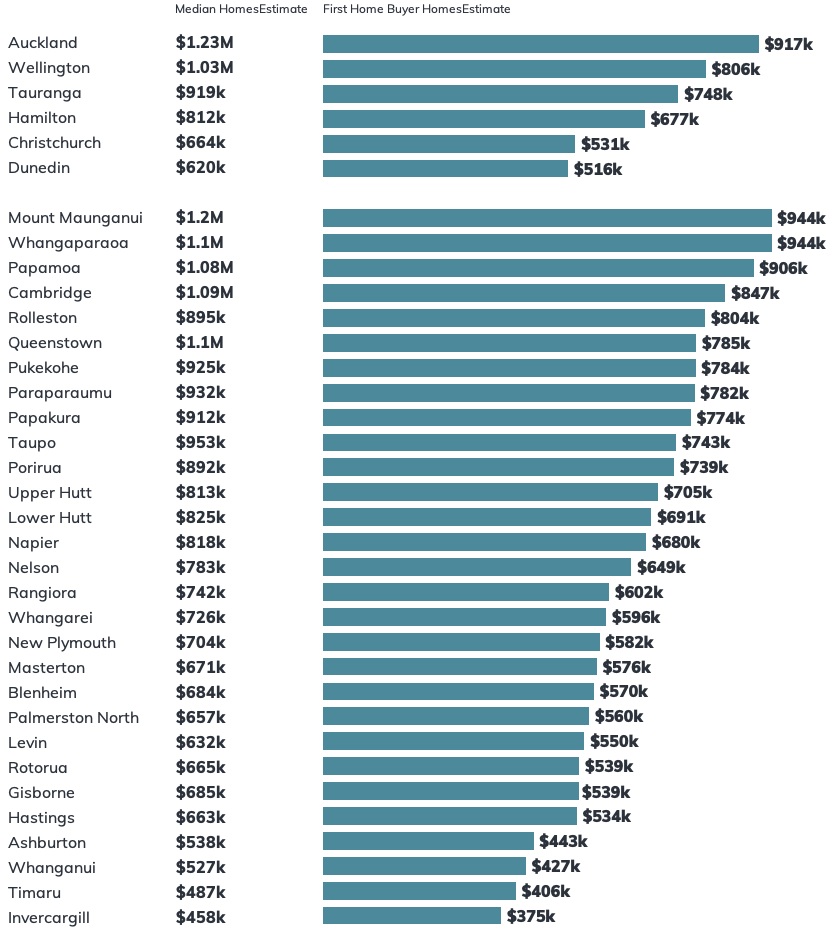

NZ’s First Home Buyer HomesEstimate

The “First Home Buyer HomesEstimate” is homes.co.nz’s estimate of what a typical first home may cost. It is calculated to be the lower quartile HomesEstimate in a town.