Homeowners take great joy in tracking the estimated value of their property on homes.co.nz, when you subtract the amount owing on your mortgage you get an idea of your equity position – this is critical if you are thinking of buying and selling anytime soon.

Your equity is the amount of your house that you own if you sold it – for most of us, it’s the money you have leftover after paying the bank.

Having equity means you can sometimes:

- Use it as a deposit for another property

- Negotiate lower interest rates

- Top up your mortgage for debt consolidation, renovations or other big purchases

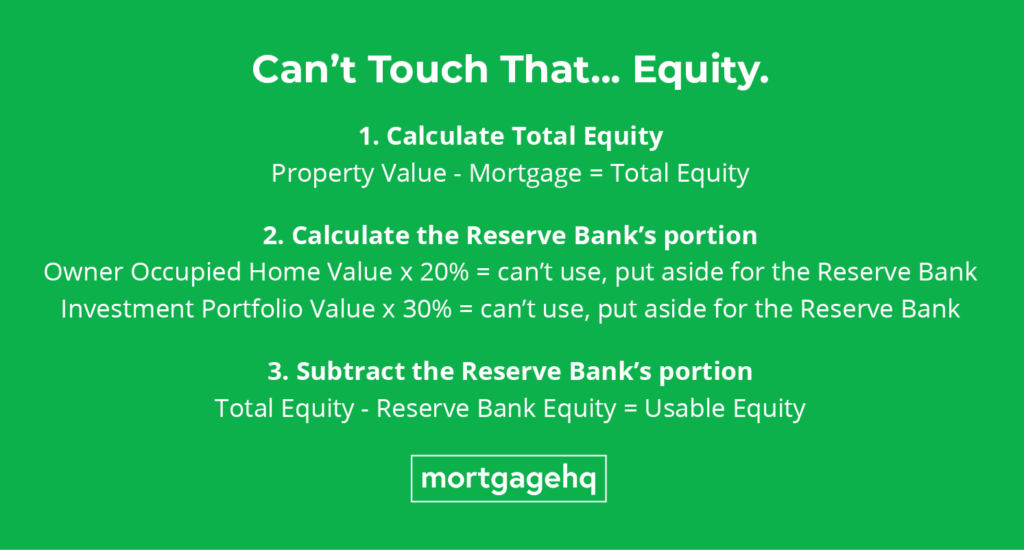

To calculate equity the formula is simple: House Value – Mortgage Amount = Equity

But don’t forget the Reserve Bank of New Zealand has some rules that banks have to follow most of the time. The main guidelines are:

- Your owner-occupied home needs to have 20% equity

- Your investment properties need to have 30% equity

What this means is that not all of your equity is yours to use immediately. Where these calculations can get confusing is when you are trying to understand the equity you have available to use right now without selling your house. Income permitting, you can borrow up to 80% of the value of your family home or 70% of your investment portfolio. For you to understand your immediate options, you need to calculate your usable equity.

What number should I use?

- To track your net worth and wealth-building progress, use total equity. Especially if the market is flat as the value may not increase fast, but your equity will increase as you pay down your mortgage.

- To discover your immediate options, use usable equity. This equity is available for you to use in a variety of situations by restructuring your mortgage.

To get help calculating these numbers try the online Mortgage Snapshot – it takes 90 seconds and gives you a lot of useful information.

PS. If your goals require a more aggressive lending strategy, outside of the RBNZ’s rules, mortgage advisers have access to ‘non-bank lenders’. Clients find this a lifesaver for aggressive property investment or to save their home after finding themselves in financial strife.